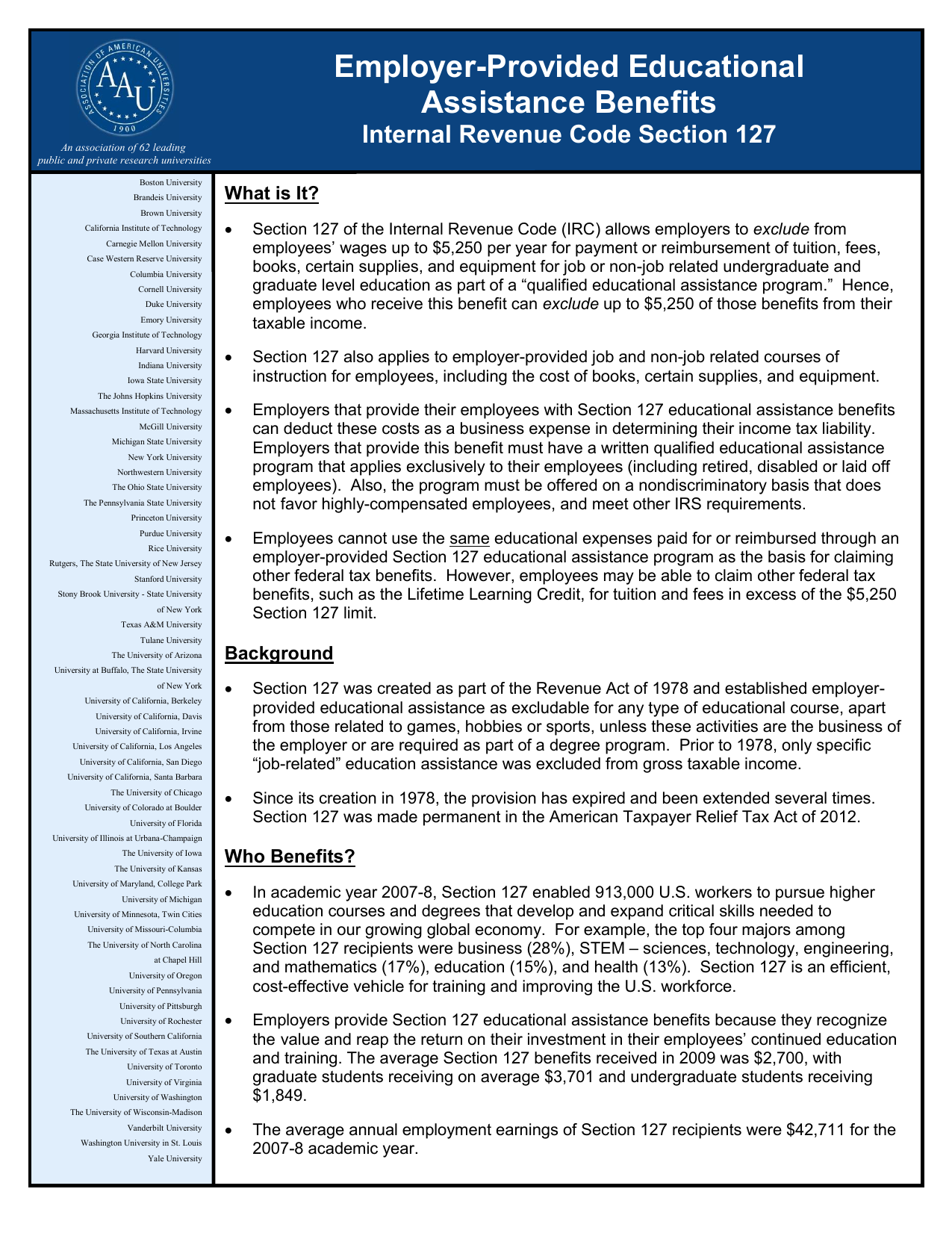

Section 127 Income Tax

Section 127 Employer Provided Educational Assistance Benefits

Briefing On Tax Free Student Loan Repayment Peanut Butter Student Loan Assistance

Section 127 Capital Gains Tax Income Tax In The United States

Https Willamette Edu Offices Hr Pdf Benefits Tuition Tuition Pdf Taxability 20info Pdf

Http Www Citadel Edu Root Images Human Resources Forms Graduate Tuition Waiver Faqs Pdf

Irs Section 127 Employer Provided Pdf Free Download

20 1996 110 stat.

Section 127 income tax. Appeal to the commissioner appeals. A benefit an employer provides on behalf of an employee is taxable to the employee even if. More than one irc section may apply to the same benefit. Amounts for additional education expenses exceeding 5 250 may be excluded from tax under irc section 132 d.

1 any person dissatisfied with any order passed by a commissioner or a taxation officer under section 121 122 143 144 162 170 182 183 184 185 186 187 188 or 189 or an order under sub section 1 of section 161 holding a person to be personally liable to pay an amount of tax or an order under clause f of sub section 3 of section 172 declaring substituted for treating by finance act 2003 a person to be the. Section 127 in the income tax act 1995 127. The secretary of the treasury shall establish expedited procedures for the refund of any overpayment of taxes imposed by the internal revenue code of 1986 which is attributable to amounts excluded from gross income during 1995 or 1996 under section 127 of such code including procedures waiving the requirement that an employer obtain an employee s signature where the employer demonstrates to the satisfaction of the secretary that any refund collected by the employer on behalf of the. Section 127 of the income tax act 1961 act for short deals with the power of competent officers to transfer cases.

Expatriate posts based on the requirements of the ipc rdc. For example education expenses up to 5 250 may be excluded from tax under irc section 127. The secretary of the treasury shall establish expedited procedures for the refund of any overpayment of taxes imposed by the internal revenue code of 1986 which is attributable to amounts excluded from gross income during 1995 or 1996 under section 127 of such code including procedures waiving the requirement that an employer obtain an employee s signature where the employer demonstrates to the. There will also be a layak menuntut insentif dibawah seksyen 127 which refers to claiming incentives under section 127 of the income tax act ita 1976.

This is incentives such as exemptions under the provision of paragraph 127 3 b or subsection 127 3a of ita 1976 which is claimable as per government gazette or with a minister s approval letter. Tax exemption of statutory income for 10 years under section 127 of the income tax act 1967 act 53 dividends paid from the exempt income will be exempted from tax in the hands of its shareholders ii an approved ipc rdc status company will enjoy the following benefits. 1 power to transfer cases 2 999999. 104 188 title i 1202 c 3 aug.

Https Www Irs Gov Pub Irs Tege Rr54 305 Pdf

Section 127 Capital Gains Tax Income Tax In The United States

2

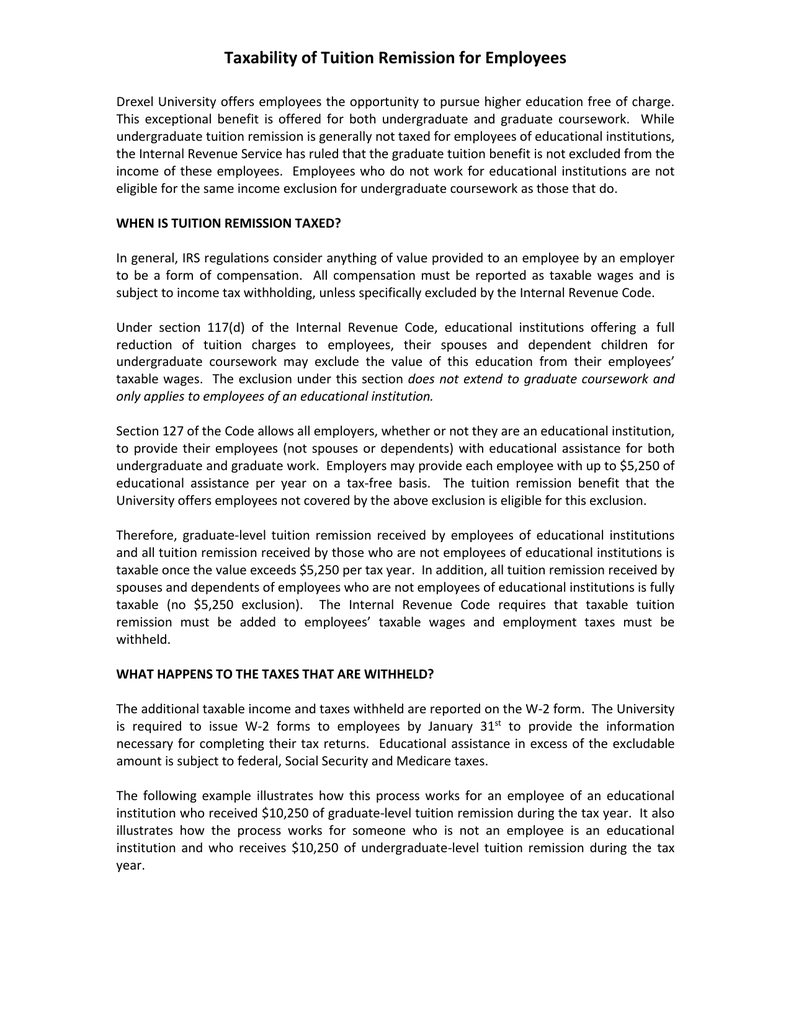

Taxability Of Graduate Tuition Remission For Drexel University

Https Drexel Edu Media Files Comptroller Payroll General Tuition 20remission 20taxability Ashx La En

Taxability Of Tuition Remission For Employees

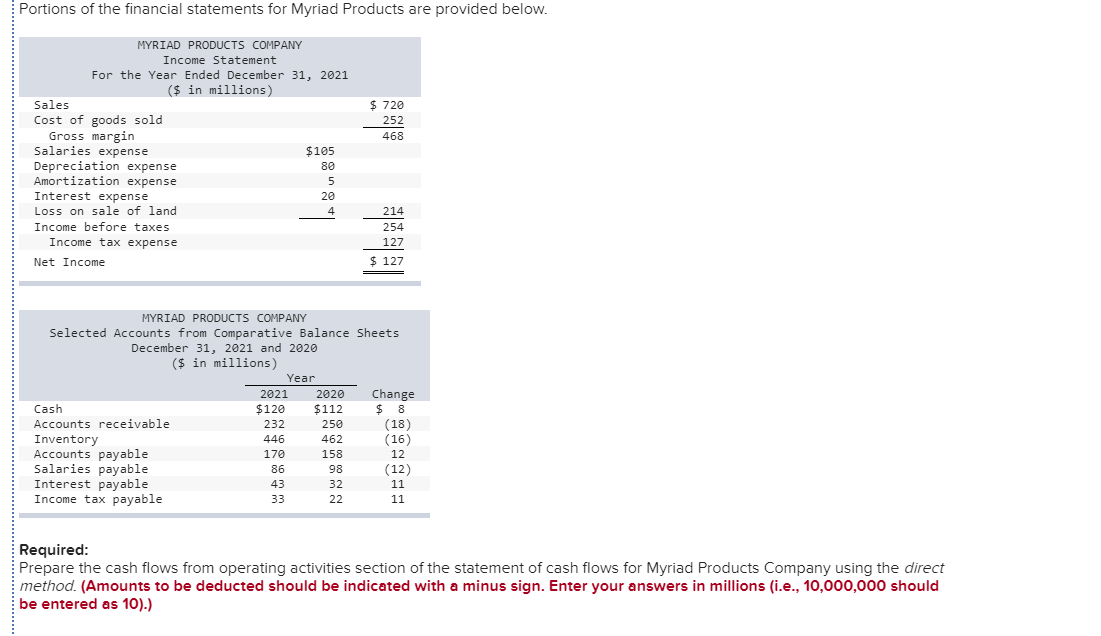

Solved Portions Of The Financial Statements For Myriad Pr Chegg Com

2

Content Malaysian Industrial Development Authority

2

Solved Guess By Ateeq Nomi Bro

Https Www Cupahr Org Wp Content Uploads Mawpp Fidelity Investments Fidelity Sd Er Assistances Cares 20act Pdf

Fed Inc Tax Outline 1 Summary Taxation Of Individual Income Studocu

2

2

040825 Aicpa Educati The Gateway To The Us Labor Market

Https Www Bakermckenzie Com Media Files Insight Publications 2015 04 New Tax Incentives In The Malaysian Budget Files Read Publication In English Fileattachment Al Malaysia Newtaxincentives Apr15 Pdf

Https Pdf4pro Com Cdn Akta Cukai Pendapatan 1967 Akta 53 Pindaan 2ab541 Pdf

Starbucks College Achievement Plan Program Document Pdf Free Download

Https Fairtax Structure Psyclone Netdna Ssl Com Client Assets Fairtaxorg Media Attachments 56c4 Abfe 6970 2d07 Aa0d 0000 56c4abfe69702d07aa0d0000 Pdf 1455729662

E Filing File Your Malaysia Income Tax Online Imoney

Never Filed Income Tax Before Here S A Simple Guide On How To Do It Online World Of Buzz

Https Www Nacubo Org Media Nacubo Documents 127davissupport Ashx La En Hash 86bb2c9751eb0cbd0f71d8ab4c72339b3c75c4ad

Domestic Direct Investment Ddi Initiatives Miti

2

Solved 3 200 1 150 Interest Income Gain On Sale Of Eq Chegg Com

Sy Lee Co Update Income Tax Restriction On Facebook

T Y 2016 Grounds Of Appeal Under Section 127 Against Order Issued 122 5a I T O 2001 Appeal Prejudice Legal Term

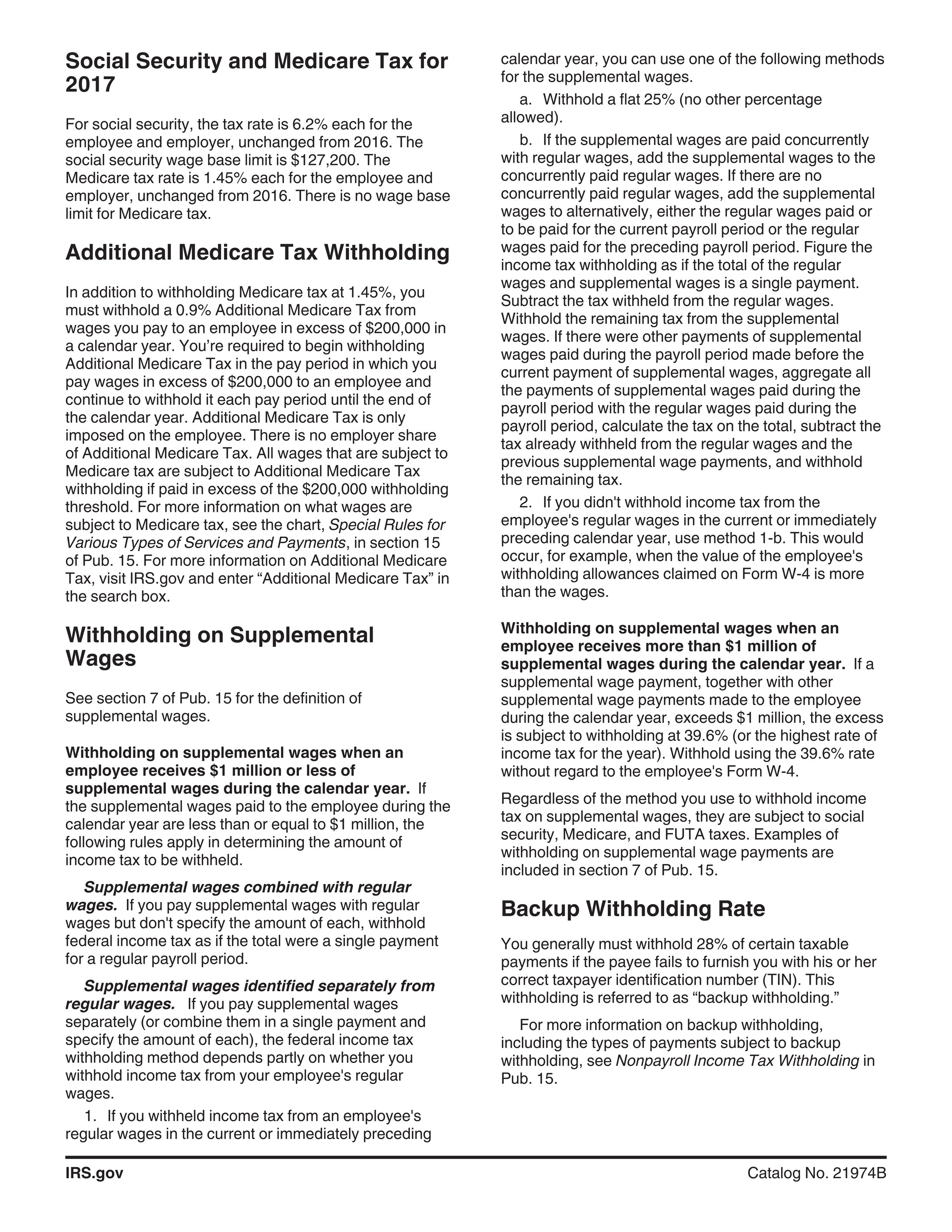

Early Release Copy Of 2017 Percentage Method Tables For Withholding Published Current Federal Tax Developments

2011 Form Dc D 40ez D 40 Fill Online Printable Fillable Blank Pdffiller

2

Congress Reaches Agreement On A Coronavirus Relief Package Tax Aspects Of The Cares Act

Leadership Exchange Summer 2014 Page 34